Are you looking to file your company tax return but worried about making serious mistakes, it is important to be prepared. Lodging your taxes can be overwhelming, and even small mistakes could cost you money or lead to penalties. Taxgain, a leading provider of effective accounting, tax administration and advice in Sydney, is here to help you avoid these common mistakes so you can lodge the company tax return with confidence and money on taxes.

1. Applying Tax Losses Incorrectly

If your business had losses in past years, you might be able to use these to reduce your tax bill. However, there are rules about when and how you can use these losses. If you don’t follow these rules, the ATO may not allow the losses, and you could lose tax benefits.

Example: If your business suffered losses in 2023 and you try to offset them against profits in 2024 without meeting the conditions set by the ATO, you could end up paying more tax.

How to Fix This: Check the ATO’s requirements for using tax losses or ask for our professional help. We can ensure that your business meets these requirements and gets the most benefit from any tax losses.

2. Missing Out on Deductions You Can Claim

Many businesses don’t claim all the tax deductions they are eligible for, which could save them money. Deductions like home office expenses, travel costs, and training for staff can reduce your taxable income if you claim them correctly. Sometimes, businesses either don’t know about these deductions or don’t have the right paperwork to back up their claims.

Example: If you buy a new laptop for work but don’t keep the receipt, you might not be able to claim it as a business expense later.

Actionable Advice: Keep all your receipts and documents for anything you think could be a deductible expense. Good record-keeping helps you claim everything you’re entitled to. Our professional team can advise you so you can make the most of your deductions.

3. Misusing the Instant Asset Write-Off

The Instant Asset Write-Off allows businesses to claim deductions on certain purchases. However, the $ limit keep on changing yearly. You need to make sure your assets qualify and that you follow the rules for business use.

Example: If you buy a car for business and claim a full deduction without checking if the car is used only for work, the ATO might reject your claim.

How to Avoid This Mistake: Understand the rules for asset deductions. Our expert accountants can guide you on which assets qualify and how to claim them properly.

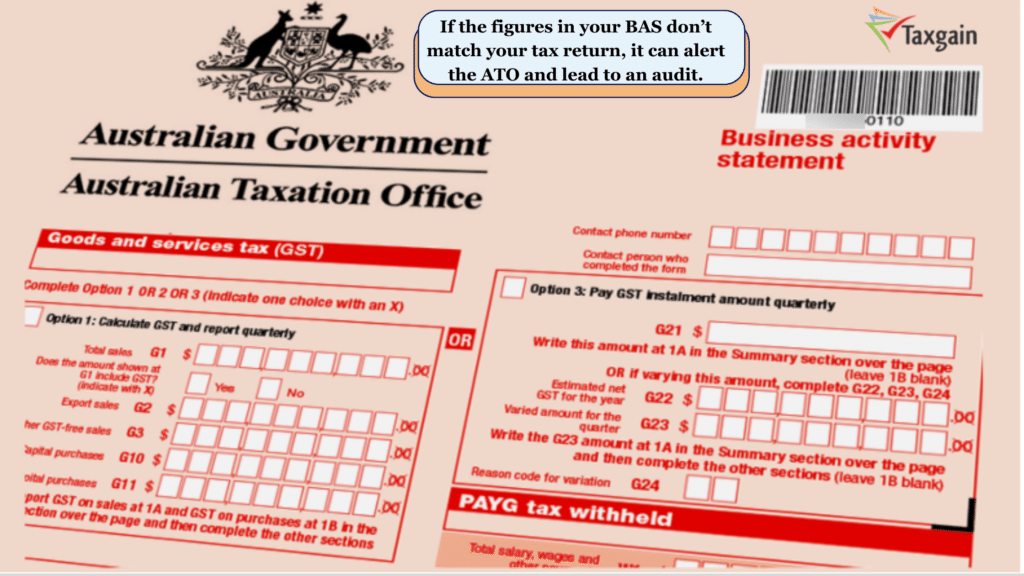

4. Not Reconciling BAS (Business Activity Statements) Correctly

Reconciling your BAS with your company tax return is crucial. If the figures in your BAS don’t match your tax return, it can alert the ATO and lead to an audit.

Example: If you report different GST amounts in your BAS compared to your tax return, the ATO may ask for an explanation, causing delays or penalties.

Solution: Regularly check and match your BAS and tax return figures. At Taxgain, we can help you do this, so your numbers are accurate and consistent.

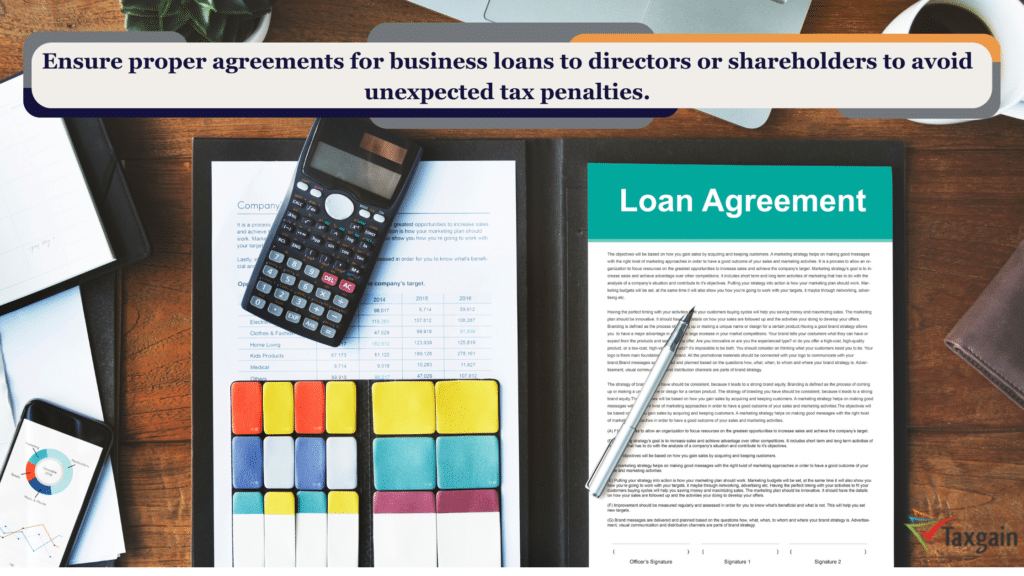

5. Not Having Proper Loan Agreements with Related Parties

If your business loans money to directors or shareholders, you need to have Div 7A loan agreements in place complying with ATO requirements. If you don’t follow the rules, the loan could be treated as a dividend, leading to unexpected taxes.

Example: If a director borrows money without a written agreement and doesn’t pay it back on time, the ATO could classify it as income, which means higher tax for the director.

Tip: Always have written loan agreements that include repayment terms. Taxgain can help set up these agreements and ensure they comply with ATO rules.

6. Not Reporting Foreign Income and Investments

If your business has income or investments overseas, you must report them accurately. sometime businesses miss this or incorrectly calculate AUD income from overseas, which can cause serious problems if the ATO audits later on.

Example: If your company has a foreign investment that earns income and you don’t declare it, the ATO may impose heavy fines.

How to Fix It: Make sure all foreign income and investments are recorded properly. Taxgain can help you manage these details and stay on the right side of the law.

7. Not Being Prepared for an ATO Audit

If the ATO decides to audit your company tax return, it can be stressful if you don’t keep appropriate documents for lodged returns. The ATO might check your records, deductions, and income. If they find any mistakes, they could fine your business or charge extra tax.

Example: If you claim deductions for expenses but don’t keep receipts, the ATO could disallow the deductions, resulting in a higher tax bill.

Tip: Keep detailed records of all your transactions, income, and expenses. Taxgain ATO audit for you, ensuring your you don’t pay fine/penalty.

Conclusion

Filing your company tax return doesn’t have to be stressful. By avoiding these common mistakes, you can save money and stay compliant with tax laws. If you need help filing your tax return, reach out to Taxgain. We’re here to make the process simple and hassle-free. Contact us today to get the expert tax planning for your company tax return.